May 1st, 2024: UPDATE: New Annuity Rates Released and IMPROVED.

1-888-58-FACTS Annuity Facts

Stress

less

about

your

wealth

Welcome to AnnuityFacts.com!

We are a network of independent annuity specialists who are licensed in all 50 States. Our team helps consumers shop the entire annuity market place and compare all of the Fixed Annuities, Equity Index Annuities (EIA) and Single Premium Immediate Annuities (SPIA) side-by-side through one source.

We help clients drill down on the fine important details all the annuity companies on our proprietary side-by-side quoting system. This comparison tool gives our clients a good one page visual that helps them judge for themselves which annuity they feel is best for themselves. To learn more about our company’s history and story click here.

What Are Annuities?

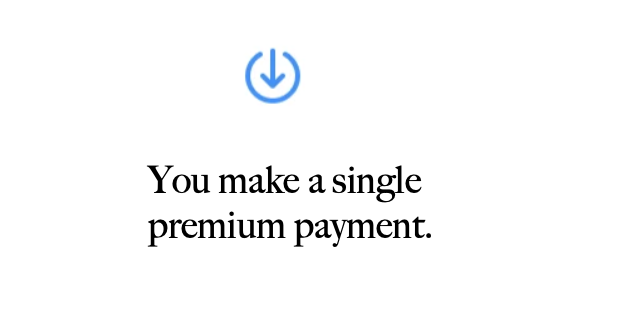

Fixed and index annuities are a contract between you and an insurance company, in which you make a lump sum premium payment to set up your contract. In return, the insurance company agrees to protect your principle from market losses. Your money grows at either a fixed stated rates or you can index your money to various indexes.

There are some annuities that even pay you a guaranteed life time income stream or you can always walk away lump sum with your full contract value with no fees after a selected number of years. Annuities also offer tax-deferred growth on your interest and include a death benefit that will pay your beneficiary your full principle plus gains — less any withdrawals.

If you would like to have the top ten annuity companies compared side-by-side prepared by one of our licensed agents FedEx’d to you fill in the quick contact info form below.