How do Income Annuities work?

An income annuity serves as a lifetime income guarantee purchased from an insurance company to mitigate the risk of outliving your retirement savings. Similar to insuring your home, it’s a means of insuring your longevity by transferring the risk of outliving your assets to the insurance company.

Funding an income annuity can be done through various methods — whether it’s years before retirement, at retirement, or over time. Regardless of the funding approach, the primary benefit remains consistent: a dependable, guaranteed income stream throughout your retirement years. This stream simplifies your retirement spending and provides the assurance that your savings won’t be depleted prematurely. Conceptually, it’s akin to purchasing a pension for yourself.

While all annuities share this fundamental principle, they can become intricate due to additional features and complexities that may obscure their value. At Blueprint Income, we specialize in providing straightforward solutions, focusing solely on income annuities (such as immediate annuities, longevity annuities, and Qualified Longevity Annuity Contracts) and fixed annuities. These products offer clear guarantees — either a guaranteed income or a guaranteed return — in exchange for your investment. They’re transparent in what they offer and represent the most cost-effective means of obtaining a guarantee.

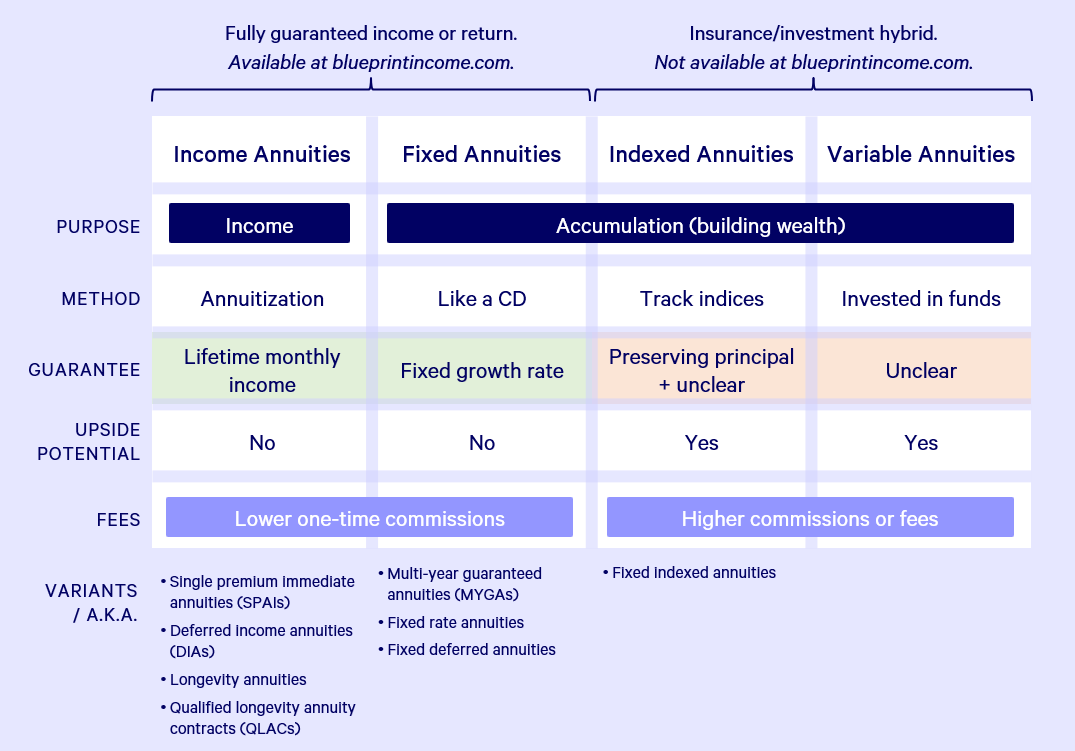

Here’s a breakdown of the various types of annuities available:

Deciding on an Income Annuity: Is It the Right Choice for You?

Considering an income annuity might be a prudent step if:

- You find that the combination of your Social Security and pension benefits falls short in meeting your day-to-day living costs,

- You’ve already begun putting away funds for your golden years,

- You enjoy robust health and anticipate a longevity that’s above the norm, or

- You’re looking to bolster the predictability of your retirement finances.

It’s essential to recognize that annuities serve as one piece of a broader retirement strategy, rather than the entire solution. They’re not designed to mirror the high returns of the stock market, nor do they typically adjust for inflation.

For those aiming to reduce the risk of depleting their retirement funds while also enhancing the financial legacy they leave, studies suggest that portfolios which leverage annuities over bonds tend to forecast more favorable outcomes. Dive into our findings on optimizing retirement portfolios by reading further here.

Exploring the Varieties of Income Annuities

Income annuities come in three distinct forms, each offering a reliable and guaranteed stream of income for life with differences in the commencement of payments and the financial resources used for their initiation. The trio of income annuity categories includes:

- Immediate Annuities: Ideal for those on the cusp of retirement or already enjoying their post-work years, these annuities start disbursing funds within the first 12 months of purchase.

- Longevity Annuities: Suited for individuals who are still some years away from retiring, longevity annuities promise income that begins over a year after the purchase date.

- Qualified Longevity Annuity Contracts (QLACs): Tailored for retirees aiming to delay Required Minimum Distributions from Traditional IRAs, QLACs are a type of longevity annuity offering payouts that commence post age 73 and before 85.

Discover complimentary estimates for each income annuity type using our Online Income Annuity Quote Tool. Continue reading for a comprehensive understanding, financial illustrations, and in-depth insights into each income annuity variant.

| Type | Immediate Annuity | Longevity Annuity | QLAC |

| Starts | Within 1 year | In more than 1 year | In more than 1 year, after age 73, and by age 85 |

| Provides | Guaranteed income for the rest of your life | Guaranteed income for the rest of your life | Guaranteed income for the rest of your life |

| Funded With | Qualified (IRA) or non-qualified (personal savings) money | Qualified (IRA) or non-qualified (personal savings) money | Only qualified money (Traditional IRA or 401(k) rollover) |

Securing Your Income Annuity in the Digital Age

Purchasing an income annuity with Annuity Facts has entered the digital realm. With our innovative platform, you can obtain instant quotes and complete your application for the insurer entirely online, bypassing traditional face-to-face appointments and paper forms. We’re fully licensed in all 50 States and offer these services and our team is at your finger tips via chat, email, or phone to offer tailored support.

Follow these steps to acquire your income annuity online:

- Utilize the Income Annuity Quote Tool to get complimentary quotes.

- Take your time to consider the specifics of the annuities and the quotes provided.

- Not ready to purchase immediately? Secure your rate with the “Lock Quote” option for 7-14 days. Remember, to benefit from these secured rates, the insurer must accept your completed application before the quote’s expiry.

- Our dedicated team will touch base to verify your details and manage the submission of your application to the insurer(s).

For any inquiries or guidance, our customer service team is ready to assist you. Simply fill in the form below to get started today!